Ahead of tomorrow's CPI, traders are eyeing this morning's Producer Prices for any hints that the disinflation trend will return…or not.

The answer is "not!"

April Producer Prices rose 0.5% MoM (vs +0.3% exp), with March's +0.2% MoM revised down to -0.1% MoM. The downward revision did not stop the YoY read rising to 2.2% (from +2.1% in March)…

Source: Bloomberg

This is the highest YoY read since April 2023 and is the fourth hotter than expected headline PPI print…

Source: Bloomberg

Producer Prices have been aggressively downwardly revised for 4 of the last 7 months…

Source: Bloomberg

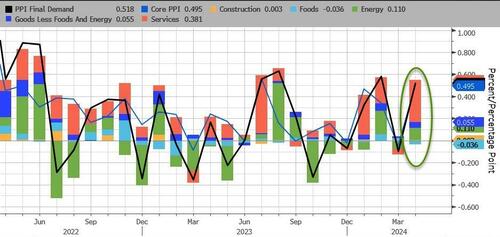

Services costs soared, dominating April's PPI gains while Energy was only a secondary impact…

Source: Bloomberg

After last month's farcical 'seasonally adjusted' gasoline price, April saw the PPI Gasoline index rise (with actual prices at the pump) but still has a long way to go…

Source: Bloomberg

Core PPI was worse – rising 0.5% MoM (more than double the +0.2% MoM expected) – which pushed the Core PPI YoY up to +2.4%…

Source: Bloomberg

And finally US PPI Final Demand Less Foods Energy and Trade Services rose by 0.4% MoM and 3.1% YoY (the highest in 12 months).

Worse still the pipeline for primary PPI is not good as intermediate demand is starting to accelerate…

Source: Bloomberg

So, no, The Fed does not have inflation under control.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Stellar

Stellar  Litecoin

Litecoin  VeChain

VeChain  Maker

Maker  Zcash

Zcash  NEO

NEO  Decred

Decred  0x Protocol

0x Protocol  Ontology

Ontology  OMG Network

OMG Network