Two weeks ago, we laid out the various reasons why – according to JPMorgan and Goldman – sentiment on US consumer stocks had cratered, and would continue to worsen.

Indeed, after a brief short squeeze at the end of September, the XRT retail ETF is at the lowest level since June after peaking on the "last Fed hike" in late July, and as we enter into 4Q, there is a lot on the line in the consumer space.

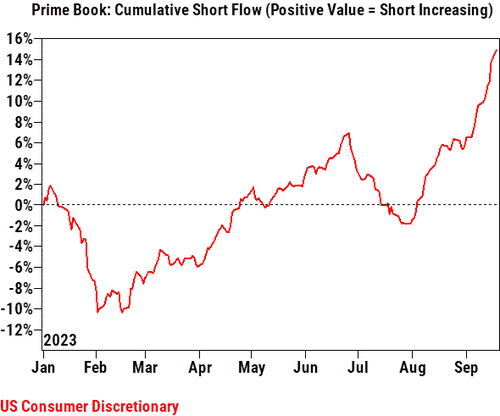

As Goldman's Prime Brokerage recently noted, shorting in the consumer discretionary space is at YTD highs as a result of a growing multitude of macro issues.

Here courtesy of Goldman consumer trader Scott Feiler, are some of the biggest concerns in focus about the health of the consumer as we start 4Q, ranked by time to see if they ultimately become bigger issues or not:

- Oil (3Q-4Q focus): We won’t have to wait long, daily average gasoline prices have ticked back lower the last few days and remain in focus. This will be an ongoing debate, though tough to sort out from student debt and the other headwinds.

- Slower September Consumption Trends (October/November focus): Should find out in November, companies spoke to an expected lull post back-to-school, which we’ve seen, but most seemed to expect an acceleration again back into the holidays.

- Student Debt (October/November focus): Should find out in November if this drives a sustained slowdown, or just a temporary one in October.

- Consumer Credit (6-12 month focus): This will probably take at least 6 months. NCO’s and DQ’s will go higher, it just is a question if they continue to outpace normal seasonal levels, which they have been doing

- Employment (2024 focus): This does not feel like it will aggressively break (just a modest cooling to continue), nor be decided in the very near future.

- GLP-1 (2024 focus): Restaurant and Food stocks have underperformed significantly, in part due to GLP-1, among other concerns (disinflation). As part of Jason English’s reiteration of his buy rating on HSY this morning, he argues that relative to 2019, volume trends for overall snack foods and confection have been stable since May. Rather than the beginning of a new secular trend, he sees a delayed deflation of a Covid consumption spike. By 2023-end most snack food categories are on track to have mean-reverted back below the pre-Covid volume trend line with the undershoot best attributed to price elasticity.

We may not have to wait that long. To get a more accurate and real-time snapshot of how the consumer is doing as we enter the critical final quarter of the year, chock-full of spending holidays, we go straight to the source: card spending data reported by three large banks: Bank of America (full report here for pro subs), Barclays (full report here) and Citi (full report here).

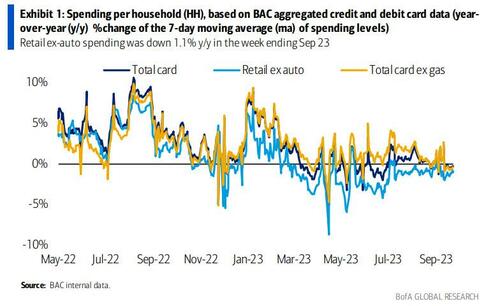

Starting with BofA, we get an ugly if not catastrophic snapshot of the health of consumer spending, to wit:

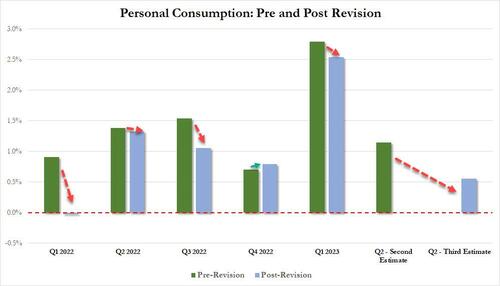

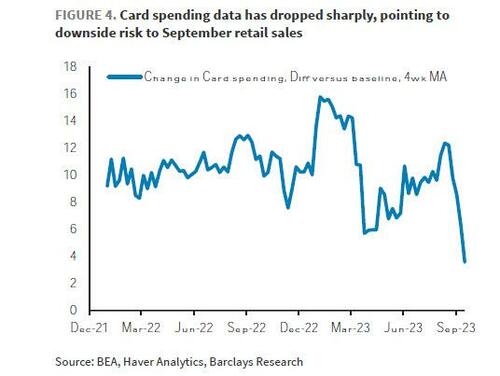

Next, we go to Barclays whose card spending data paints a far more dire picture. Coming just days after we learned that the BEA had significantly overestimated recent economic growth…

… Barclays writes in its latest Global Rates Weekly note (available here), that real-time data on card spending has taken

another leg lower and is significantly weaker than prior levels (Figure 4).

This, the bank warns, "points to a potentially weak retail sales print in September, though that is scheduled to be released two weeks from now (Oct 17)."

Finally, we go to Citi (full report available to pro subs), where the card spending data is downright recessionary.

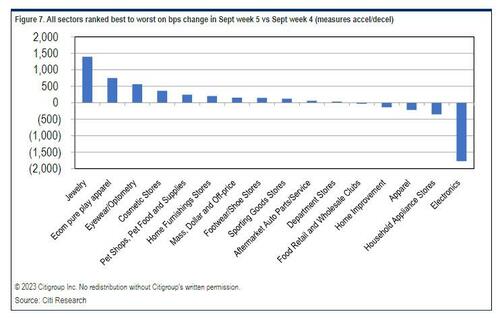

As the bank's retail analyst Paul Lejuez writes, Citi's credit card data "for the 16 sub-sectors we track show that total spending in Sept wk 5 (ended 9/30) decreased 11.3%, a deceleration compared to Sept wk 4 (ended 9/23), which was -10.9%. Ex Food spending was -10.6% in Sept wk 5 vs -10.2% in Sept wk 4. The month of September was -10.8% (-10.9% ex-food), which is the now weakest month of the year, dethroning August which was -10.2% (and -10.4% ex-food)."

Here are the strongest and weakest sub-sectors: Cosmetics (+3.9%), Pet Shops (+1.9%), and Eyewear/Optometry (+1.4%). We saw the largest declines in Aftermarket Auto Parts/Service (-16.0%), Household Appliances (-15.9%), Home Improvement (-15.1%), Ecom Pure Play Apparel (-14.3%), Food Retail (-12.6%), Electronics (-12.3%), Jewelry (-11.8%), Apparel (-11.6%), Home Furnishings (-10.5%), Dept Stores (-9.5%), Sporting Goods (-8.4%), Footwear (-6.7%), and Mass/Dollar and Off-price (-4.6%).

Courtesy of Lejuez, here are several most notable call-outs in Sept wk 5:

And while the report's punchline is bad enough, namely that "September marks the fifth consecutive month of spending"…

… one look at the heatmap says it all: the US consumer has finally hit the brick wall.

So for those who still hope that the Fed may hike one more time in November: don't.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Stellar

Stellar  Litecoin

Litecoin  VeChain

VeChain  Maker

Maker  Zcash

Zcash  NEO

NEO  0x Protocol

0x Protocol  Decred

Decred  Ontology

Ontology  OMG Network

OMG Network