With manufacturing surveys still in contraction, and underlying components screaming stagflation as orders drop and prices pop, all eyes are on the 'bigger' Services sector surveys this morning which are expected to slip lower in August (but remain in expansion – above 50).

The S&P Global US Services PMI disappointed, declining from 52.3 (July) to 50.5 (final August), and below the 51.0 preliminary August print – weakest since January

BUT

The US ISM Services soared from 52.7 to 54.5 (well above the 52.5 exp) – strongest since February

Source: Bloomberg

In case you wonder why these surveys can be so completely opposed, it is survey responses like this…

A Real Estate worker said that:

A Government worker said that:

So a total joke with surveys pointing in completely different directions, but the message was similar under the hood with prices soaring…

Source: Bloomberg

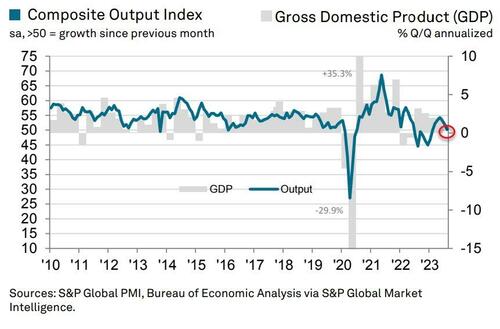

The final S&P Global US Composite PMI Output Index posted 50.2 in August, down from 52.0 in July, to signal only a fractional increase in business activity at US private sector firms. The slowdown in growth stemmed from a weaker service sector expansion and a renewed decrease in manufacturing output.

Not a pretty picture:

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said:

It looks like we're gonna need more 'Bidenomics'.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Stellar

Stellar  Litecoin

Litecoin  VeChain

VeChain  Maker

Maker  Zcash

Zcash  NEO

NEO  Decred

Decred  0x Protocol

0x Protocol  Ontology

Ontology  OMG Network

OMG Network