Authored by Mike Shedlock via MishTalk.com,

Not exactly timely, Bloomberg notes “The widening gap between gross domestic income and gross domestic product is a worrying signal.”

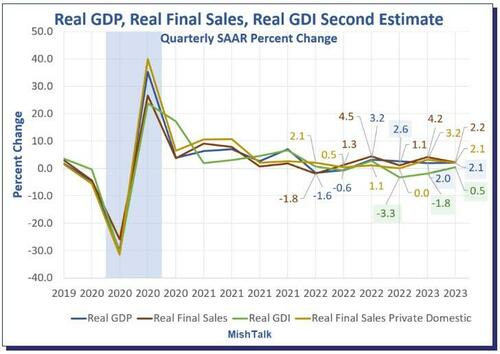

GDP vs GDI Chart Notes

-

Real means inflation adjusted

-

GDP is Gross Domestic Product

-

GDI is Gross Domestic Income

-

Real Final Sales is the bottom line assessment of GDP. It excludes inventories which net to zero over time.

GDI was negative for two consecutive quarters and has been weaker than GDP for four quarters. GDI is now positive, but it is subject to greater revisions than GDP.

GDP numbers from the BEA, chart by Mish

Bloomberg opinion columnist Aaron Brown says Summer’s End Is Ushering In a Recessionary Chill, emphasis mine.

I have been talking about the GDP vs GDI discrepancy, negative revisions, the discrepancy between jobs and employment, corporate profits, and the job leverage ratio for months, and in far more detail. Let’s take a look at some of my recent posts.

Negative Revision to 2nd Quarter GDP, Huge Discrepancy with GDI Continues

The lead chart and the second chart are from my post Negative Revision to 2nd Quarter GDP, Huge Discrepancy with GDI Continues

Real GDI peaked in the third quarter of 2022.

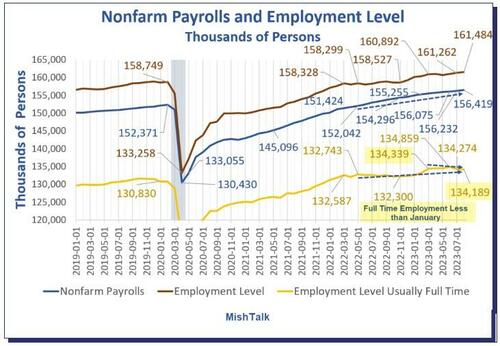

Discrepancy Between Jobs and Employment

Employment levels and jobs data from the BLS, chart by Mish.

Payrolls vs Employment Gains Since May 2022

-

Nonfarm Payrolls: 4,377,000

-

Employment Level: +3,185,000

-

Full Time Employment: +1,446,000

-

Only 45.4 percent of the employment gains for the last 15 months was full time employment.

Jobs Rise by 187,000 But 110,000 Negative Revisions and Unemployment Soars by 514,000

On September 1, I noted Jobs Rise by 187,000 But 110,000 Negative Revisions and Unemployment Soars by 514,000

Full time employment is down by 150,000 since January of 2023.

Here is a blurb I have posted in my monthly jobs reports for eight straight months.

The monthly jobs report by the BLS samples a mere 6 percent of jobs. The Quarterly Census of Employment and Wages (QCEW) payroll employment data represents 95 percent of the data.

The BLS will not incorporate March of 2023 until January of 2024. Lovely.

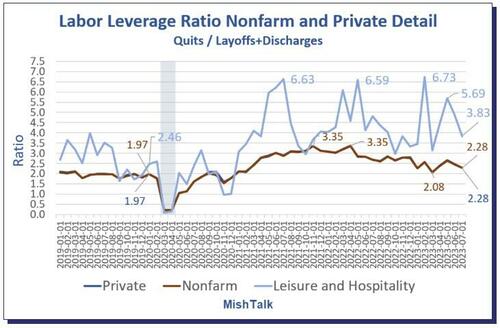

The Labor Leverage Ratio, a Measure of Wage Bargaining Power, Is in Retreat

Data from the BLS, the Labor Leverage Ratio (LLR) is defined as Quits / (Layoffs + Discharges)

The BLS comments “the quits rate can serve as a measure of workers’ willingness or ability to leave jobs.”

The LLR is a refinement to the quits rate.

I have commented on labor leverage several times this year, most recently in The Labor Leverage Ratio, a Measure of Wage Bargaining Power, Is in Retreat

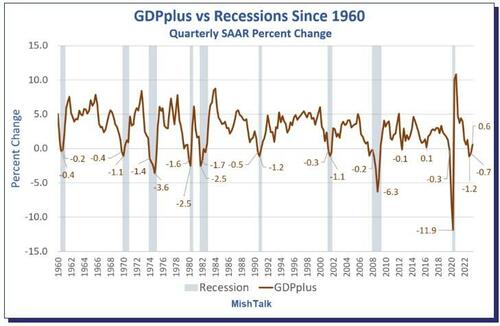

Philadelphia Fed GDPplus Measure Sure Looks Like Recession Started in 2022 Q4

The Philadelphia Fed has a measure called GDPplus that’s a blend of GDP and GDI, not an average. It appears to lean more heavily on GDI.

In 100 percent of the cases, with no false signals, no misses, and no lead times more than two quarters, every time GDPplus had two consecutive quarters of negative growth, the economy was in recession.

On closer inspection, all but once, and the exception was a mere -0.1 percent, every time GDPplus had one quarter of negative growth, the economy was or would soon go into recession. By soon, I mean within two quarters.

GDPplus accurately forecast the 1961 recession but GDP and GDI both did.

GDPplus Recession Signals

Mish compilation of recession lead times based on DGPplus data

GDPplus Recession Signals Synopsis

-

GDPplus signaled every recession

-

GDPplus was on time 4 times, early by a quarter 3 times, and early by 2 quarters twice.

This makes it appear as if GDPplus is a leading indicator. It isn’t because the data is heavily revised.

The BEA makes revisions frequently, especially on GDI. Since GDPplus is more reliant on GDI, it also has significant swings. However, GDPplus is the best recession indicator yet.

One quarter is sufficient and barring positive revisions to GDI and by implication GDPplus, the economy went into recession in the fourth quarter of 2022.

For more discussion of GDPplus, please see Philadelphia Fed GDPplus Measure Sure Looks Like Recession Started in 2022 Q4

Mainstream media is finally waking up to these discrepancies, albeit without any detailed analysis.

It’s quite possible a recession has come and gone. The NBER already had one instance of declaring a recession after it was over so don’t be surprised if it happens again.

It’s possible that a recession has come and gone with an interlude due to Inflation Reduction Act inflationary Nonsense.

If so, expect a rare double dip.

* * *

Subscribe to MishTalk Email Alerts.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  Stellar

Stellar  Litecoin

Litecoin  VeChain

VeChain  Maker

Maker  Zcash

Zcash  NEO

NEO  0x Protocol

0x Protocol  Decred

Decred  Ontology

Ontology  OMG Network

OMG Network